Dependent care is expensive! Like the Child Tax Credit, a Dependent Care Flexible Savings Account, or DCFSA, is a taxpayer benefit for parents (and also in this case, taxpayers who have non-spouse adults who depend on them). Goodness knows, we need it!

If you’re familiar with a medical Flexible Spending Account (FSA) or Health Savings Account (HSA), you may already have a good idea of what an FSA essentially is. Just in case you haven’t, we’re going to start this article with an explanation of what an FSA is in general. After that, we’ll cover the tax savings you get with an FSA. We’ll wrap up this article by getting into the downsides of an FSA, along with our recommendations.

What Is a Dependent Care FSA?

A DCFSA is an account that enables you to use pre-tax dollars to cover important dependent care expenses. It’s flexible in that you can use the money to pay different eligible expenses to different eligible recipients at different times. You can’t just pay your oldest child $50 to babysit for a night out using your FSA. Specifically, babysitting is only eligible if it’s for work purposes, and besides that, you are not allowed to use it to pay someone who is a dependent of yours for tax purposes even if it is for work.

What you can do with a DCFSA is pay a person or organization for a variety of different kinds of care for your children or other eligible dependents while you work. After-school programs, au pairs, babysitters, daycares (for adults or children), elder care, extended care, nannies, and other kinds of similar services as listed on this webpage are eligible if they are for an eligible dependent.

Make sure to keep your receipts! You will be expected to prove that you paid for dependent care if you want to be able to pay for it tax-free.

DCFSA Tax Savings

The advantage of a DCFSA is tax savings. To oversimplify things, if your marginal tax rate is 22%, you will save twenty-two cents on every dollar spent using an FSA in lieu of paying it with a regular payment method.

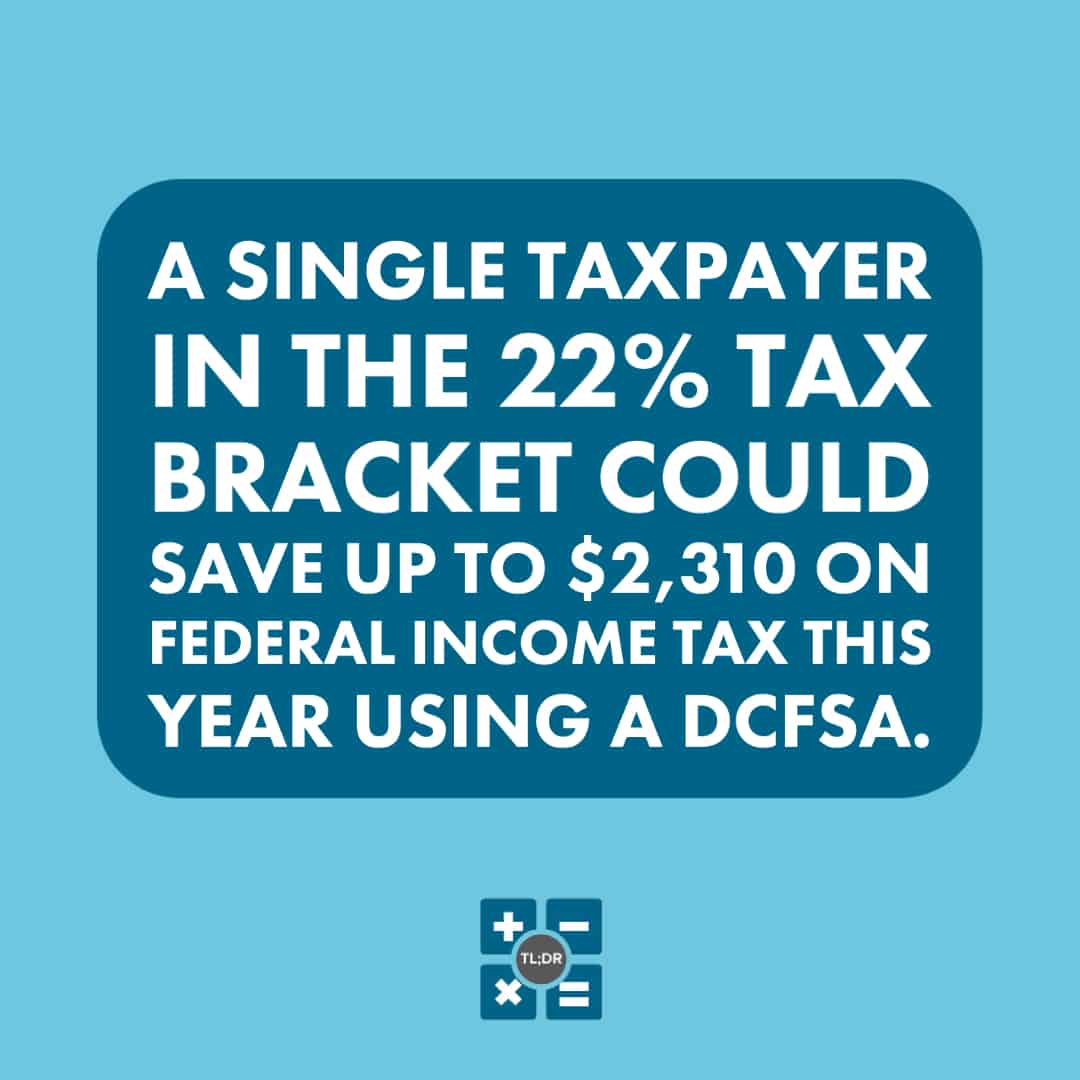

Thankfully, the DCFSA limits have recently been raised! These limit increases are fantastic because, in many places — especially in Washington State — child care can easily cost $10,000 for a single child. For single and joint taxpayers, the maximum for a DCFSA is $10,500 (up from $5,000), and it’s $5,250 (up from $2,500) for married individuals filing separately. This means that a single taxpayer in the 22% tax bracket could save up to $2,310 on federal income tax this year using a DCFSA.

The Downsides of a DCFSA

If a DCFSA can save you thousands of dollars a year, what are the downsides?

One major downside of the DCFSA program as a whole is that it’s up to your employer whether or not they want to make this benefit available to employees. If you don’t have an employer, as in, you are an independent contractor or unemployed, the option simply isn’t available to you.

If you are able to sign up for a DCFSA, there’s a second minor disadvantage to doing so: administrative paperwork. You have to get a Tax ID for your care provider and you have to regularly submit receipts to your FSA program for the expenses to be eligible.

We recommend making a digital copy of every receipt from your care provider ASAP for two reasons: 1) you probably have to do it anyway to upload the receipt to the FSA web portal, and 2) paper receipts can get lost easily, especially if you have one or more children in your house.

We at TL;DR Accounting are not personally invested in whether or not you choose to use a DCFSA. Our official recommendation is to use one if you are eligible. Sure there’s a bit of extra paperwork, but wouldn’t you rather have that $2,000?

TL;DR: A Dependent Care Flexible Spending Account (DCFSA) is a way for taxpayers who are employees and have one or more dependents to be able to pay for dependent care tax-free. This can save you roughly $2,000 for 2021 tax year, depending on your tax bracket and other factors. Make sure that your dependents and the recipients of the funds are eligible or you might lose those tax savings. Lastly, but also importantly, keep track of your receipts!