As a solo entrepreneur (or “solopreneur” as they say nowadays), do you feel like you’re out in the cold watching your employee friends partying inside, celebrating their juicy tax-advantaged retirement accounts? Okay, that’s a weird metaphor and it’s kind of creepy to stand out in the cold and watch people, but you get the picture. How can you, on your own, enjoy similar tax benefits as people who work for large firms and have a whole department to handle their 401(k) plans?

Though you have several different retirement options, we’re going to compare two of your best options. First we’ll cover the SEP-IRA, then we’ll touch on the Solo 401(k), and wrap up by evaluating which might be the better choice for you. Bonus: Neither of them involves stuffing cash into your couch cushions!

SEP-IRA: The Basics

SEP-IRA stands for Self-Employed Pension Individual Retirement Account. This name is sort of accurate. Yes, it is an individual retirement account for the self-employed, but calling it a pension is misleading. It does not act like a pension; it acts like what we call a “defined contribution plan,” meaning that it’s more like a savings account. Your SEP-IRA would have a dollar balance, and when that dollar balance runs out it’s over.

The SEP-IRA, as the name says, is an IRA, though a SEP-IRA does not allow Roth (after-tax) contributions. (Yes, technically you can convert your SEP-IRA into a Roth IRA, but you can’t convert it back and make more SEP-IRA contributions to it.)

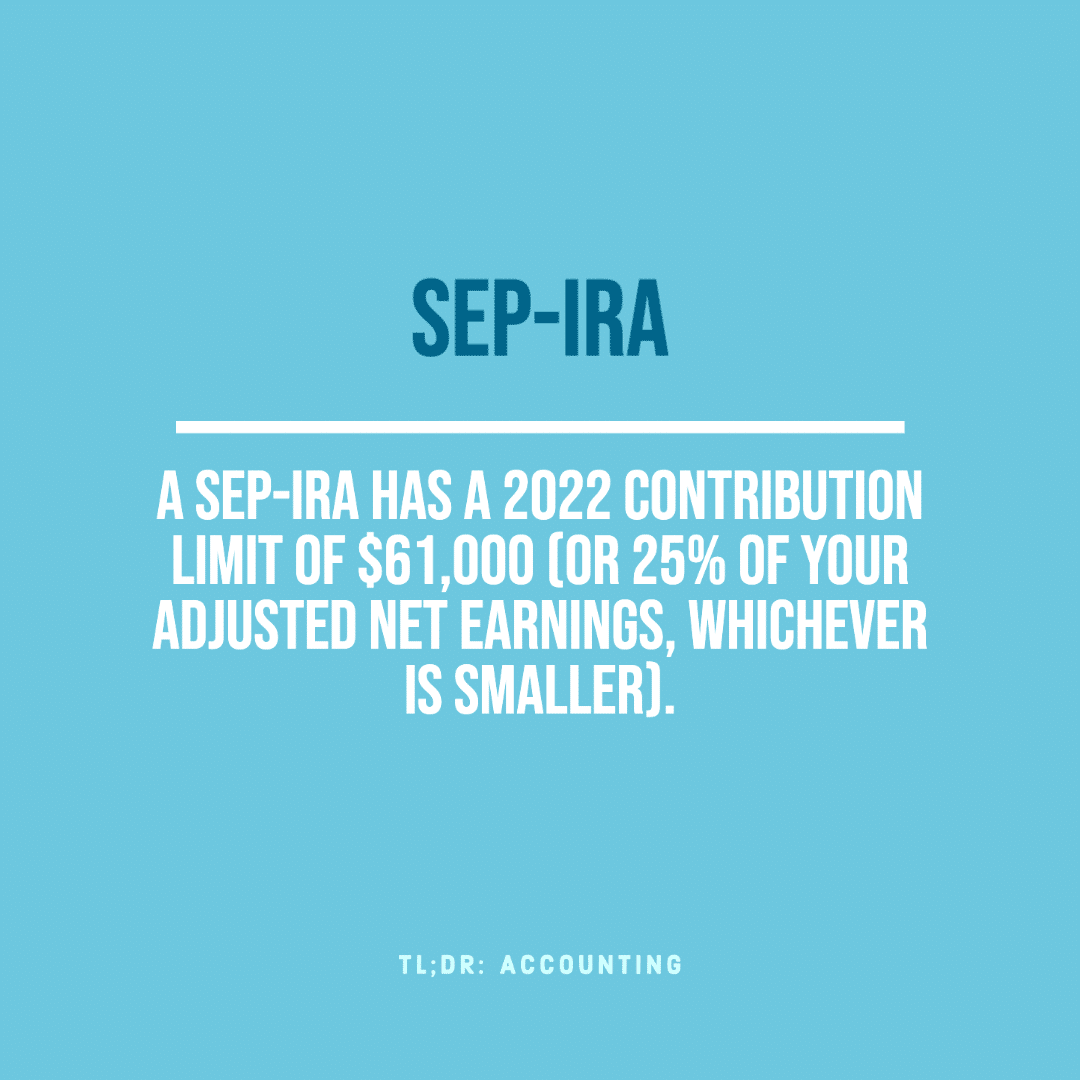

Now, why would anyone want to have a SEP-IRA if it’s just another type of IRA? The answer is contribution limits. The difference in contributions between a Traditional or Roth IRA versus a SEP-IRA are huge! Traditional and Roth IRAs have an annual contribution limit of $6,000 ($7,000 for taxpayers aged 50+). A SEP-IRA, on the other hand, has a 2022 contribution limit of $61,000 (or 25% of your adjusted net earnings, whichever is smaller).

All three types of IRA (Traditional, Roth, and SEP-IRA) are relatively simple to establish and fund. Clearly you can see why it’s worthwhile to consider a SEP-IRA if you’re self-employed!

Solo-401(k) Quick Facts

As opposed to IRAs, 401(k) plans are complex, more expensive to set up, and require much more administrative attention. The Solo-401(k) is no exception. Even so, depending on your income and goals, it might still be worth establishing a 401(k) for yourself.

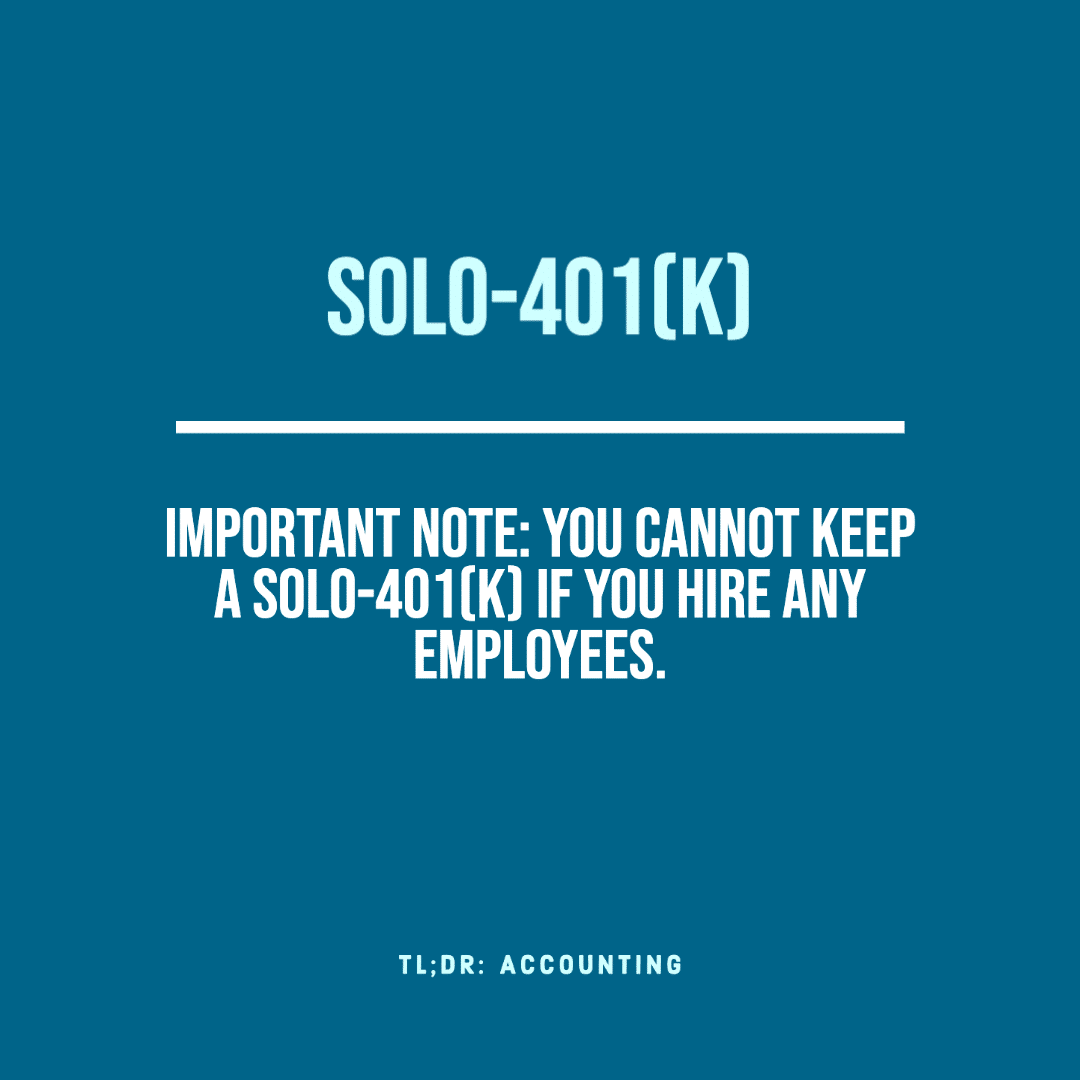

Important note: You cannot keep a Solo-401(k) if you hire any employees.

So, what makes it worth setting up a 401(k) if the plan is complex and if you’ll have to scrap it the second you hire an employee? There are several answers, but perhaps most important is the increased contribution limit. See, the IRS sets the same maximum for an employer’s funding of a Solo-401(k) as it does for funding a SEP-IRA, which is $61,000 for 2022. But with a Solo-401(k), you are acting as both employer and employee, which means you can also contribute the employee maximum of $20,500 for 2022.

Solo-401(k) plans also give you similar options to an employee 401(k). Namely, you have the option to take out a loan against your 401(k) balance, and there is an option to do a Roth 401(k) if you expect your post-retirement income taxes to be higher than they are now. Taxpayers aged 50+ have an option of up to $6,500 in catch-up contributions.

Which Is Better for You?

Both the SEP-IRA and Solo-401(k) are suitable for one-person businesses. It all comes down to whether you expect to hire an employee in the foreseeable future, your tolerance for complexity in your retirement plan, and whether you can afford and desire to contribute tens of thousands of dollars to retirement each year.

Overall, for most of our clients, we recommend a SEP-IRA for its simplicity.

We cannot quote retirement providers to you, for this you would need a retirement advisor. But we can estimate how much you might save on taxes with different types of retirement plans, and offer advice to help you achieve other financial goals as well! Contact us for more information.

TL;DR: Your two best options as a solopreneur are the SEP-IRA and the Solo-401(k). The SEP-IRA works if you hire employees and is easy and inexpensive to set up and maintain, but its contribution limits are lower. If you want higher maximum contributions you can go with the Solo-401(k), but you will lose the plan if you hire anyone, and it is complex and expensive to administer.