Q: What’s the difference between Cash and Accrual Accounting?

A: The difference is … Timing!

Okay, that’s an old borrowed joke that wasn’t that funny in the first place, but it would probably get a laugh from those accountants in the TV show Parks & Recreation.

Importantly, timing differences with regards to the operation of your business can filter through to affect the timing of when you pay taxes, the complexity of your bookkeeping, and even the accuracy of your business planning. Let’s start with an explanation of each kind of accounting, and then get into the implications at the end.

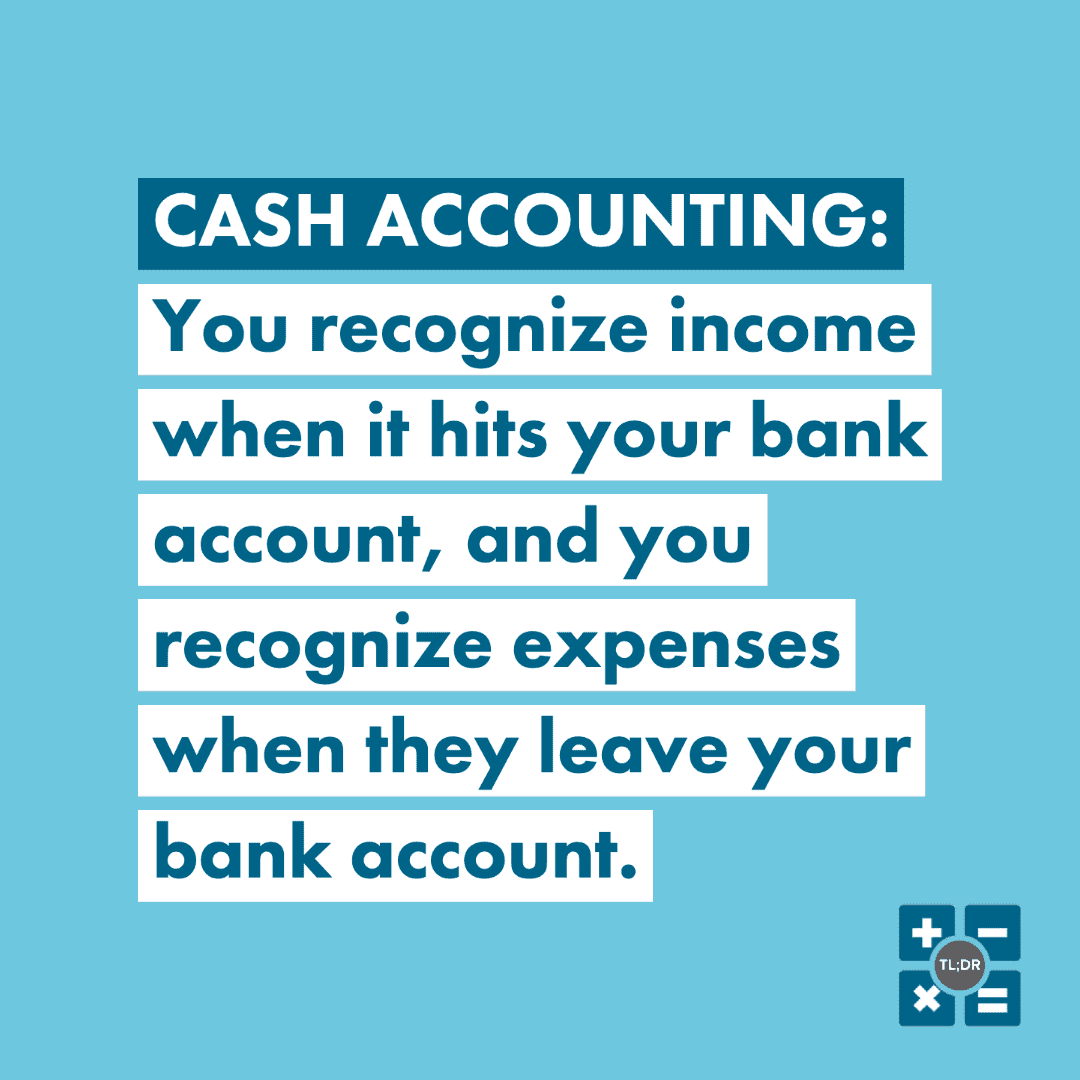

What Is Cash Accounting?

Cash Accounting is as simple as it sounds: You recognize income when it hits your bank account, and you recognize expenses when they leave your bank account. If you use QuickBooks, your QuickBooks bank balance would be the exact same as your bank balance when following the rules of Cash Accounting. But since the system is so simple, you may not need to use QuickBooks.

Under Cash Accounting, your business’s balance sheet does not have Accounts Receivable or Accounts Payable because these accounts are meant to record obligations. Cash businesses do not account for such obligations until they are met.

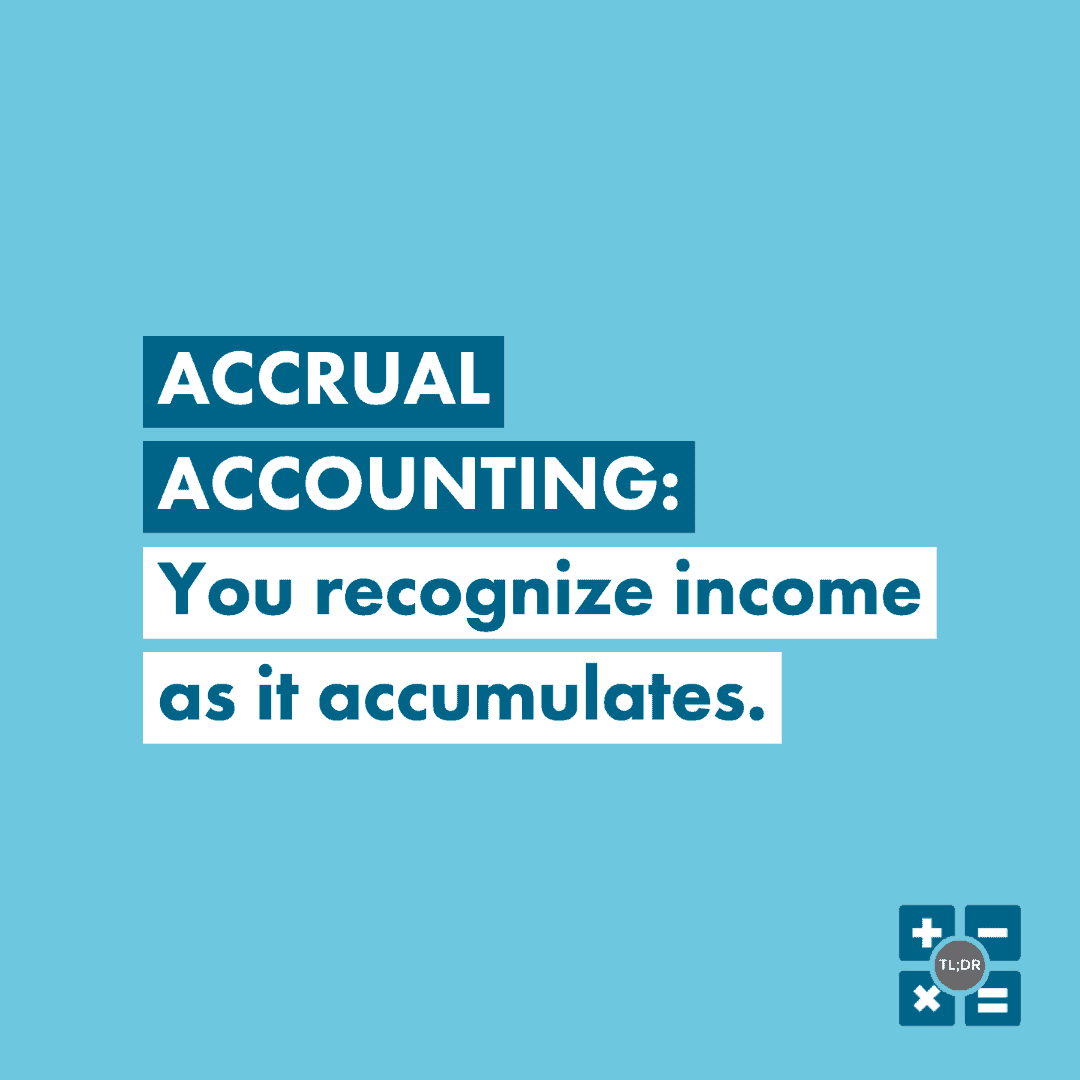

What Is Accrual Accounting?

Accrual Accounting, understandably, recognizes payment obligations as they accrue (in other words, as they accumulate). If a customer has agreed to pay you next month for some product they received today, you can immediately record an entry in Accounts Receivable equaling the dollar amount you expect to receive. At the same time, you must record Accounts Payable entries every time you purchase products or services that you will pay for later.

You almost certainly want to use some kind of bookkeeping software if you use Accrual Accounting because the bank balance that shows on QuickBooks (for example) isn’t likely to match your current bank balance on your bank’s website. This is because QuickBooks tallies up money that you owe and money that you expect to receive in order to give you a better idea of how much money you have that is available to you, after considering amounts that you owe to suppliers and amounts you have inbound.

Cash vs. Accrual Accounting: Which Is Better?

Let’s get into the pros and cons of both methods.

Cash Method Pros & Cons:

- Simple bookkeeping

- The bank tracks your cash balance for you, so it’s not really necessary to reconcile

- All of the focusing on cash balance means that you have a good understanding of your cash flow

- Under the cash method, you know the current status of your business but it’s harder to see where it’s going with regards to upcoming income and expenses. This may muddy your ability to make good mid- and long-term business decisions. A good budget or forecast will solve this problem.

- You will likely find that, if you want to take out a business loan from a bank, they’ll need so many accrual-related metrics that you might as well switch over to the Accrual Method.

Accrual Method Pros & Cons:

- The accrual method keeps you focused on the profitability of your business rather than just looking at your cash balance

- It can be easier to make good business decisions when you have a good understanding of your short-term projected cash receipts and expenditures (as shown by your Accounts Receivable and Accounts Payable)

- Your bank may require you to track certain metrics in order to be eligible for a loan. Many of these metrics require you to use the Accrual Method in order to perform the calculations.

- Bookkeeping is more complex and you may need a specialist to run your books.

- It would behoove you to do a bank reconciliation every month. (Built-in pro for doing bank reconciliations: They can help you discover bank errors or fraud in your bank account).

- With this more complex accounting method, you must ensure that you don’t lose track of your immediate cash needs. If your bank balance is empty when it’s time to pay your employees and you don’t have a line of credit available, that’s a problem!

Should You Use the Cash Method or Accrual Method?

There are hybrid accounting methods that combine different elements of Cash Method and Accrual Method. Business owners with a good understanding of the nuts and bolts of both methods may want to consider going hybrid. Technically speaking, the accounting method used by the IRS to figure out your business’s income tax is a hybrid method. This partially explains why you have to fill out a bunch of forms instead of being able to have the IRS just auto-import the information it needs from your business’s financial statements.

TL;DR: The Cash Method and Accrual Method are the two main ways used by business owners and their accounting specialists to determine how well business is going. The Cash Method is simple to establish and run, which is why most business owners get started that way. However, the Cash Method becomes less useful as your business grows. Using the Accrual Method is more complex, but it gives you a much better ability to project how your business is likely to perform in future months, quarters, or years!