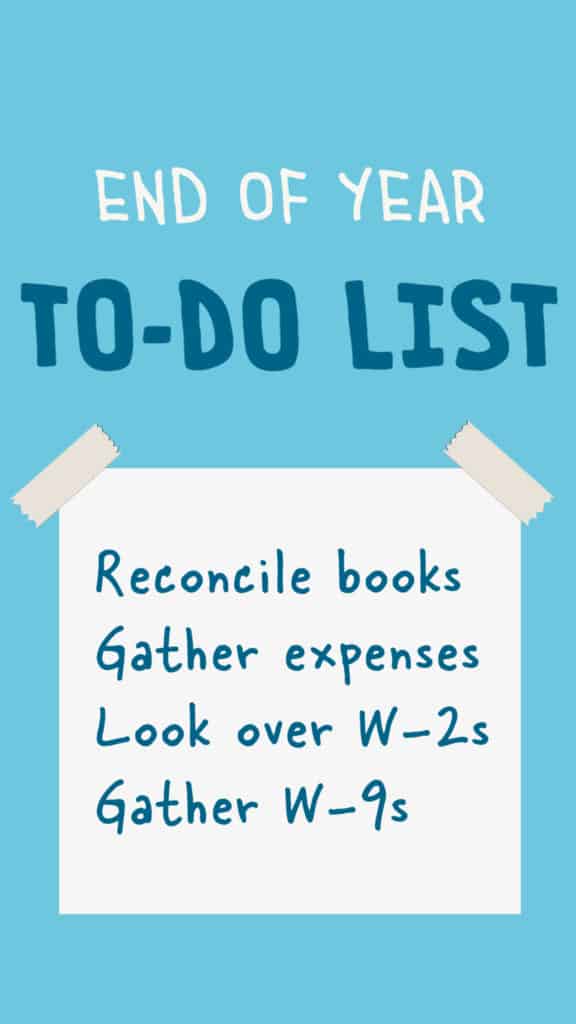

2020 has been a tough year for all of us, especially those personally affected by the COVID-19 pandemic. With so much change and so much uncertainty, it can be difficult to keep track of your business’s finances and remember to do all the things you need to do. Despite this year’s tumultuousness, there are still four very important tasks for you to take care of:

- Reconcile your books

- Gather a list of business expenses that you paid using a personal card (and vice versa)

- If you have employees, look over their W-2s for accuracy (especially when it comes to health insurance and retirement contributions)

- Gather up all required W-9s before the last minute!

Reconcile, reconcile, reconcile!

You don’t need to reconcile your books three times this month — we just said it three times because it’s that important! Though you will ideally reconcile your books at least every quarter — or, better yet, once a month — you absolutely need to reconcile annually at the bare minimum. Of course, when we say “you,” we don’t mean that you have to do it yourself: you can hire someone (like us!) to do it for you.

If you don’t know what a reconciliation is, now is a good time to learn!

How do you know that your books are accurate? Well, a great first step would be to check your bank statements to see if every transaction in your bank statements is also in your business’s books. Ideally you’ll see the same number of transactions in the same amounts, with the same starting balance and the same ending balance. It is also good to match the dates of the transactions, especially if you have multiple transactions in the same dollar amount.

Reconciliation is the process of matching your starting balance, checking off all transactions, and then identifying any “stragglers” (transactions that only exist on your books or on the bank statement, but not both). For example, if you deposited a customer’s check on the 30th, then chances are that the revenue is recorded in your company’s books but hasn’t cleared the bank yet. You can leave this transaction out of the reconciliation because it makes sense that it doesn’t match yet — you would expect it to clear the following month.

If you have a “straggler” that doesn’t seem to make sense, it may be a duplication or other erroneous entry. Do you see two transactions in your book with the same date, dollar amount, and vendor or customer name? Unless there’s a legitimate reason to get the same amount twice in one day from the same entity, chances are that it is a duplicate that should be removed. Duplicates can happen from bank transaction imports, human error, or other reasons. We at TL;DR are pros at finding and eliminating duplicates!

Most of the time, the bank statement is your “gold standard,” but it is possible that the bank may make an error. If the error is in your favor, notify them and collect on it just like in the board game Monopoly. If the bank error is in their favor, then it’s good to know about it in advance so you can avoid overdrafting on a payment once the bank discovers the error.

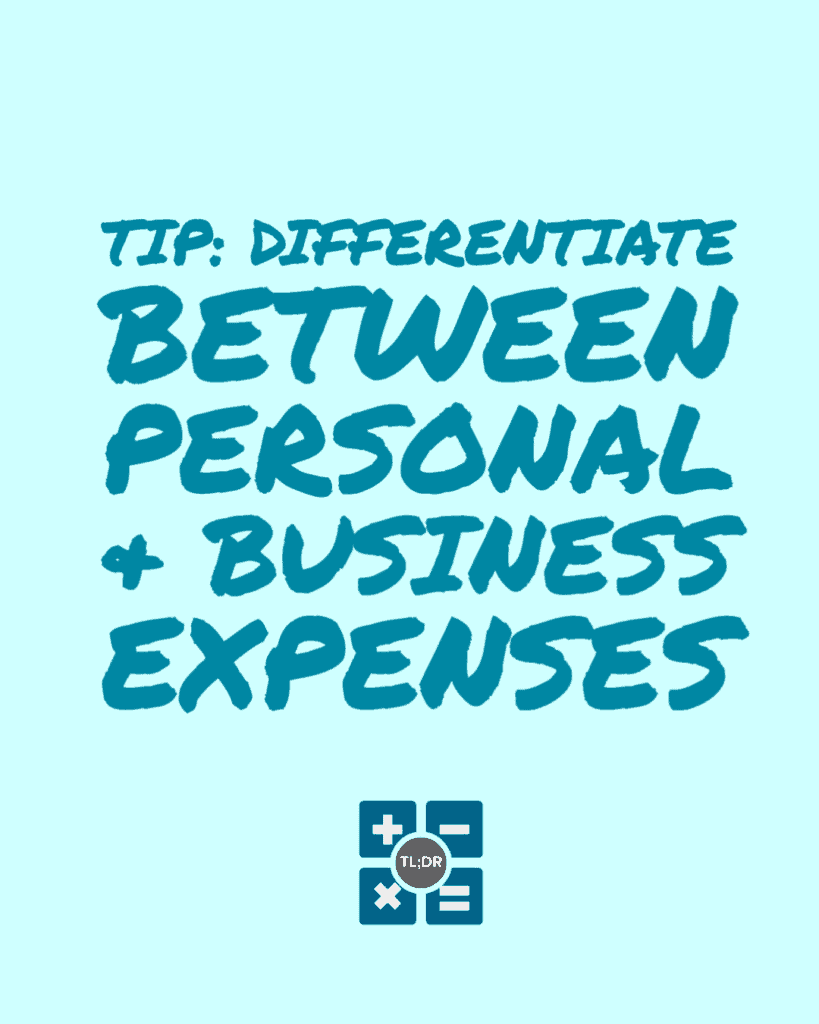

Business vs. Personal Expense Crossover

Did you have any expenses that “crossed the line” between business and personal? We’ll start off by dispensing some advice that is just good in general: Please do your best to only use your business card for business expenses and your personal card for personal expenses. It saves a lot of effort and confusion later on.

The worst case scenario when “crossing the line” is that the IRS catches some large crossed-over transactions before you can identify and correct them, and they accuse you of fraud. Regardless, if you routinely cross the line, the IRS can determine that your business is not actually a business and is really just an extension of you, and the business can lose its limited liability status. This means that a person who feels wronged by your business can sue you personally and potentially collect from your personal savings on a successful lawsuit.

Ok, now that the scary part is over, we’ll just note that there are two ideal times to separate business and personal expenses: Either immediately after they happen, or during your monthly reconciliation (see what we did there?).

What if you don’t know whether an expense is business or personal? While this is a great question for your tax professional, we’ll give you the general guideline. For an expense to qualify as a business expense in the IRS’s eyes, it has to be reasonable, ordinary, and necessary:

- Reasonable should be somewhat self-explanatory, but really it takes some intuitional judgment. Is it reasonable for a celebrity to treat hair stylist expenses as a business expense? Probably. But if you run a spork manufacturing business you probably can’t expense your hair styling unless you also star in your own spork commercials (are spork commercials even a thing?).

- Ordinary is also mostly self-explanatory. You probably know the difference between an ordinary pet and an exotic pet, especially if you’ve seen the Netflix docu-series The Tiger King. Really, a good way to know if something is ordinary is to ask yourself if a typical company in the industry would do that activity. Buying hundreds of yards of raw denim is an ordinary expense if you’re a jeans manufacturer, but it’s not ordinary if you are a clinic running blood tests (unless I’m missing something).

- Necessary is also a judgment call, but much can be revealed with a simple gut-check. Is coffee necessary for productivity? Perhaps surprisingly, the IRS feels that the answer is “yes,” and that’s why you can expense coffee supplies as office expenses. On the other hand, it’s sadly doubtful that it would be necessary to treat all your employees to a daily pedicure.

Review W-2s (if you’re an employer)

Imagine this: Employee Kat (short for Katherine) notifies your company that her W-2 is incorrect. Her Box 1 wages were overstated because her health insurance wasn’t netted out of wages, and hence she needs a W-2 correction to avoid having to overpay on her taxes. She will need a corrected W-2 (called a W2-C) because otherwise the IRS is going to compare her 1040 to her erroneous W-2 and think that her 1040 is wrong. This is an avoidable error which can be embarrassing for your company to make.

In order to avoid W-2 errors, it is highly recommended that you conduct a W-2 review before the end of each year. We are aware that W-2s are due at the end of January, which means that you can theoretically review W-2s in January. The problem with this is that you can’t make any actual changes to an employee’s wages after the end of the year; you can only correct the W-2 to match what they were paid. So if an employee was under- or over-paid last year and it’s January, your best option is to make an equal but opposite error in the coming year, and their wages will forever be “wonky” for both years in everyone’s records.

Regardless of when you do the review, there are three major dollar amounts to which you should pay close attention:

- Wages (Boxes 1, 3, and 5, which are each the same amount unless the employee is highly compensated)

- Employer-Paid Health Insurance (listed in one of the Box 12 spaces as DD)

- Retirement Contributions (Box 12, code D for a 401(k) or code S for a SIMPLE retirement plan)

- Special note: For a “SIMPLE 401(k)” plan, use Code D

Note that wages should be net wages after deducting “non-taxable compensation,” e.g. health insurance and retirement contributions. Your payroll software should provide reports to show annual income and contributions. It also behooves you to do a “sanity check.” If your employee has worked for you all year, multiply your monthly health benefit by 12 and see how it matches with Box D. If you contribute 3% of an employee’s wage to a retirement account, multiply their annual wages by 3% to see if it matches.

We’ll never tell you to “not” check certain dollar amounts, but we can tell you that if you use software to run payroll then W-2 boxes 4 and 6 are most likely correct if wages are correct. Box 2 could warrant extra scrutiny if your employee has elected to withhold extra money during the year. Lastly, while box C often stays the same year after year, it’s good to do the rounds and check if any of your employees have changed their name or moved to a new address.

The Gathering of the W-9s

A Form W-9 is a form that gives you all the information you need in order to fill out a 1099, as well as whether or not you have to fill one for the vendor in question. To start, let’s answer the question of, “Do I have to do a 1099 for this vendor:”

- Look at the federal tax classification box right underneath the business name box. If “C Corporation” or “S Corporation” is checked, then you do not have to fill a 1099 for this vendor.

- If Individual/Sole Proprietor, Single-Member LLC or Partnership is checked, then fill a 1099 for this vendor by the end of January at the latest.

- If “Limited Liability Company” is checked, then only fill a 1099 if code “P” (“Partnership”) is shown as the tax treatment.

- If the vendor checked “Trust/Estate,” then check with your tax professional.

Generally speaking, you fill 1099s for entities that are not corporations. There’s no need to request a 1099 from large chain corporations like Office Depot, Home Depot, Office Max, and Homax. On the other hand, you may not know if a local business is a corporation because individual people can legally do business under a business name. It is not safe to assume that a business is a corporation just because it has employees.

When you receive a W-9, save yourself some trouble later on and check it for completeness! We have seen W-9s missing the EIN before. This is bad because the EIN is 100% necessary for filing the 1099 later. Also, if the tax classification is missing then be sure to ask. You should not be expected to assume a business’s filing status. On the other hand, it is perfectly okay if only one of the top two boxes is filled — you need an individual’s name and/or a business name for a 1099.

TL;DR: 2020 isn’t even over yet, but we all know it’s been a rough one. Do yourself a favor and take a little extra time with your books to reconcile them and pick out any personal expenses. Check over those W-2s if you have employees, and ensure that you have W-9s from all businesses that will later need a 1099. When in doubt, ask for a W-9. Don’t feel like you’re putting them out; they are required to provide you with a W-9 upon request.