Did you know we’re on YouTube? You can watch here:

Your therapy practice is in the business of healing people. That’s awesome, and the world needs more people just like you. Keep doing what you’re doing.

That said, your finances need the same degree of care that you show your clients. Do you have an accountant, advisor, or bookkeeper to help keep track of all of this, or do you do it yourself? Developing an understanding about your finances can help you manage your own money, whether you handle it yourself or outsource that task to a professional.

Set Up a System

As a therapist, you’re probably aware that systems are one of the best ways to ensure that a task is completed consistently and reliably. Say you’re accustomed to brushing your teeth every night right before bed. On the off night that you might forget to brush, your mouth may suddenly feel stale when you lie down. This is the power of ingrained habits.

We think that you should have systems in place to track your finances. Choose one day per month to dedicate to your finances. This day should be early in the month, but after your bank has prepared your monthly bank statements. Maybe around the 5th of the month, give or take a couple of days.

TIP: Put a recurring appointment on your calendar to remind you to get this done!

On this day, you should go through your bank feed in QuickBooks Online to make sure that every item from the previous month has been assigned to a category and accepted. After this, it can be helpful to reconcile your bank account. If that sounds daunting, at least check the current bank balance in your bank feed and ensure that it matches your QuickBooks balance.

After finishing with your bank feed, pull open a Profit & Loss report for the prior month (or the prior few months) and get a feel for how much money you’re taking in and where your money is going. As you know, Net Income is revenue minus expenses, and your Net Income number is the key to the next step.

If you don’t use QuickBooks Online, you can download a handy Practice Finances Excel sheet here:

Split Up Net Income Monthly

Each month, calculate and split up your Net Income into different pots (or accounts) intended for specific reasons, such as tax savings, business savings, and retirement.

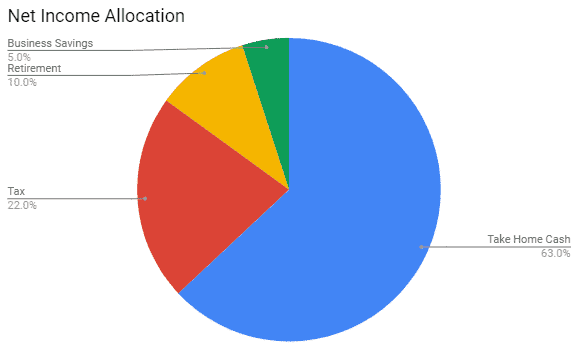

With Net Income in hand, go through this calculation: Net income = Take Home Cash + Tax 22% + Business Savings 5% + Retirement 10%

Net Income Allocation for your cash

You can do a monthly bank transfer to put your 5% into business savings, your 10% into savings for retirement, and your 22% into savings to pay for taxes. These should be in different savings accounts or sub-accounts. Each quarter you will pay in the amount in your taxes account as an estimated tax payment. Your retirement savings will stay in your savings account until year end when you will make the payment into your actual retirement account.

TIP: If your Net Income is consistent, consider setting up an auto-transfer and adjusting it on an as-needed basis.

If you’re thinking, “What about my business expenses?” then remember that this is how to divide out Net Income, which is already Revenue - Expenses. So, while it’s important to put a little money away for retirement and a rainy-day fund for your business, everything else (after taxes) is yours.

Personal Expenses

Speaking of money that is yours, how carefully are you tracking your personal expenses?

There are many popular options for completing this task, such as Mint.com, YNAB.com (“You Need A Budget”), or simply a spreadsheet in Excel or Google Sheets. If you don’t have anything set up, start it today.

In a perfect world (which may not be possible during COVID), your personal money can be spent like this:

30% to Wants (restaurants, movies, games, excursions, vacations)

20% to Desires (emergency fund, additional debt payments, extra retirement savings)

Needs and Wants

Needs are self-explanatory. If you need childcare in order to work, then that’s not really negotiable. There are many families who must pay more than 50% of their income towards needs, and if you’re in this situation then it can perhaps be a goal to one day be able to drop it to 50%.

Wants are also self-explanatory. What makes you come alive? Live your passions, and enjoy putting your hard-earned money towards what you truly love in life.

Desires

Desires need a bit of explanation. As opposed to Needs and Wants, we think that there are clear priorities for your Desires portion. In short: You need an emergency fund. We’ll say it again: You need an emergency fund! This is money that will keep you fed and paying rent if something bad were to happen. It could also be used towards co-pays and coinsurance if you are in an accident of some kind.

The “golden rule” for an emergency fund is 3 months of your living expenses (the “Needs”). Some recommend saving up to 6 months in an emergency fund, but this is your choice. A good starting point is one month of expenses as you work toward building up to 3 months of expenses. It might take you some time to build up your savings but it is so relieving to have the money on hand when something unexpected comes up.

After your emergency fund is established, we recommend that you attack your debt relentlessly. You’ve already put that 10% of net income towards retirement and socked away money for your emergency fund, so the next priority is cutting down your interest expense by paying down your principal amount of debt. Naturally you should go after the highest-interest debt first to save yourself the most money. A different way to pay off your debt is to rank it according to the amount owed. This way you tackle the smallest balance first, knocking whole accounts down until it is gone. Once you pay off your first debt, you can use that money to increase payments to all your other debts.

If you’re debt free, then first off, congratulations. Chances are very good that you’ve been in debt at some point in your life, especially if you went to college. Being debt-free is quite an achievement, and you can celebrate this by putting more money into retirement. Sure you could work forever, but do you really want to?

TL;DR: Do you have a system to manage your business finances? Do you have a system to manage your personal finances? You should have both, and the time to set these up is now! Imagine how happy you will be a year from now, patting yourself on the back for setting clear boundaries instead of letting the money slip through your fingers.

Good News! We're holding a free webinar to help! We'll teach you how to put aside money for taxes, manage inconsistent income & plan for retirement. You can learn more here:

Khaled joined TL;DR as Principal in December of 2022, and has quickly hit the ground running offering a fresh new perspective for the TL;DR team and clients. He’s a natural entrepreneur & leader, starting his days at 4 AM with a nice cup of coffee to get a jumpstart on projects before the business world wakes up. His one piece of advice to business owners? Ask yourself if you are creating just another job or a business. Ideally, you should be building something that doesn’t require you to be there 40 hours a week!