Perhaps you’ve seen that familiar list of business entities: Sole proprietorships (i.e. doing business as yourself), partnerships, LLP’s, LLC’s, PLLC’s, LLLP’s, C Corporations (or just “Corporations”), and S-Corporations.

An important thing to note about the S-Corporation business entity is that the whole point of choosing to be an S-Corporation is a tax decision. We call it “electing to be taxed as an S-Corporation.” There’s a section in the tax code called subchapter S that gave us the name S-Corporation.

So, an S-Corp is a corporation that has elected to be taxed differently from a normal corporation. In short, it’s what we call a “flow-through entity” which means that while you have to file an S-Corporation tax return (Form 1120-S), the S-Corp does not pay any taxes. When you file your own taxes, you tack on any S-Corporation income that “flowed through” to your personal tax return.

What it really boils down to is: if you become an S-Corporation, will you save enough money in taxes to make it worth the time, money, and complexity involved with incorporating?

S-Corporations can be solo operations, partners in a partnership, members in an LLC, shareholders in a C Corporation, and many other things. However, there are a few things they cannot do, which we will cover below.h

| Table of Contents: Accounting For S Corp |

|---|

| Pros and Cons of S-Corporations |

| When You Should Not Be an S-Corp |

| How to Become an S-Corp |

| What Are the Rules You Must Follow as an S-Corp? |

Pros and Cons of Accounting for S-Corp

Pros:

- You can save a lot of money on taxes, because you don’t have to pay self-employment taxes (roughly 15% tax) on the portion of your share of profits that is not considered salary. You can also possibly access better health insurance options as a corporation than as an individual.

- As a flow-through entity, S-Corporations don’t have to pay double taxation. Double taxation is something C Corporations have to pay, and it means that income distributions from a C Corporation are taxed twice on their way to your bank account (once on the corporate side, and once again on your tax return). This “pro” is only in comparison to a C Corporation.

- Like other formal business entities, S-Corporations offer liability protection. If something goes wrong and your business is sued, then claims can’t be made against your personal property (house, savings, etc) unless:

- You have not respected the boundary between your personal and business expenses.

- You have personally guaranteed a loan. Fortunately, this only allows the lender to claim your personal assets, not just anybody suing your business.

Cons:

- As the owner of an S-Corporation you will become an employee of your own business, even if it’s a solo operation. Be your own boss! This is a “con” because you are expected to determine a reasonable salary for yourself, and that reasonable salary is subject to payroll taxes.

- Who determines what “reasonable” means? Unfortunately, as an S-Corp you may end up in the situation of explaining to the IRS why your salary is reasonable.

- Payroll. Even if you haven’t hired any employees, as an S-Corp you are now your own employee, which means you have to file payroll, pay payroll taxes, and file quarterly payroll reports. This can take a lot of time, especially if you haven’t run payroll before. Or you can outsource your payroll and spend money instead of time.

- Formality. On the scale of not-formal to extremely formal, S-Corps are on the formal side. This means articles of incorporation, shareholder meetings with minutes, corporate officers with positions like President and Treasurer, regular required business form filings with the government, and filing fees. These are the same requirements for being a single-member LLC.

- You are taxed on your share of the income of the S-Corporation, even if you leave the income inside the company. Many owners of S-Corps take distributions in order to pay income taxes, but keep in mind that large distributions can lead you to accidentally break loan agreements with banks — many loan agreements have provisions on how much money you’re allowed to pull from your business.

- Looking at the longer term, you can only have up to 100 shareholders and they all have to be US Citizens or resident aliens. Also, you can only have one class of stock — you can’t do common and preferred stock, for instance.

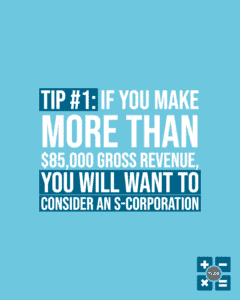

TL;DR: It all really boils down to money. Will being an S-Corporation save you money? (Do you make more than $85,000 / yr?) If so, go for it! If not, consider becoming an LLC instead for the liability protection. We can help you determine if becoming an S-Corporation will pay for itself in tax savings.

When You Should Not Be an S-Corp

Before you jump to corporate inception, there are some situations and reasons that would turn an S-Corp election into a dealbreaker.

S-Corp Dealbreakers:

- We’ll start off with the simplest dealbreaker: money. If your business is still a small operation, then there’s a chance that after all the corporate origination fees, government filing fees, and tax preparation fees, there just isn’t that much tax saved. We recommend making at least $85,000 in revenue per year before considering s-corporation election.

- You can’t have foreign shareholders. If foreign investment is important to you, then steer clear of S-Corps.

- Complexity. Even if being an S-Corp will save you some money, you must follow specific S-Corp rules. You might decide that it’s not worth the shareholder meetings, minutes, tax forms, payroll, and government filings. If this is all too much for you, consider being a sole proprietor.

- Incorporating is a one-way street. Once you become an S-Corporation, the only major entity type change you can make after that is to change to a C-Corporation (or dissolve and liquidate the company). You can’t change to an LLC, partnership, or anything else like that. If you’re still hemming and hawing about entity type, you can stay a sole proprietorship or partnership indefinitely. Just know that you don’t get liability protection until you change to a corporation or LLC. If you are becoming an LLC making the S-Corporation election you have to wait 5 years before you can ‘undo’ it.

- If you own real estate and rent it out, this is called passive income. If you have passive income, then you don’t have to pay payroll taxes on it. BUT, if you become an S-Corp then you will be expected to pay yourself a salary, effectively converting a portion of your income into income that you have to pay payroll taxes on. This can lose you money!

Tl;DR: If you become an S-Corporation, will you gain money, lose money, or break even? Check with us! If you don’t like complexity, payroll, or business formality, if you might want foreign investors, or if your business is a rental real estate business, then an S-Corp is probably not for you. In that case consider becoming an LLC.

How to Become an S-Corp

So you’ve decided that you want to become an S-Corp. What do you do now? Well, you can’t go wrong by contacting us for advice, but here’s an overview of the steps to become an S-Corporation. (If you are already an LLC in Washington State you can skip down to Step 8.)

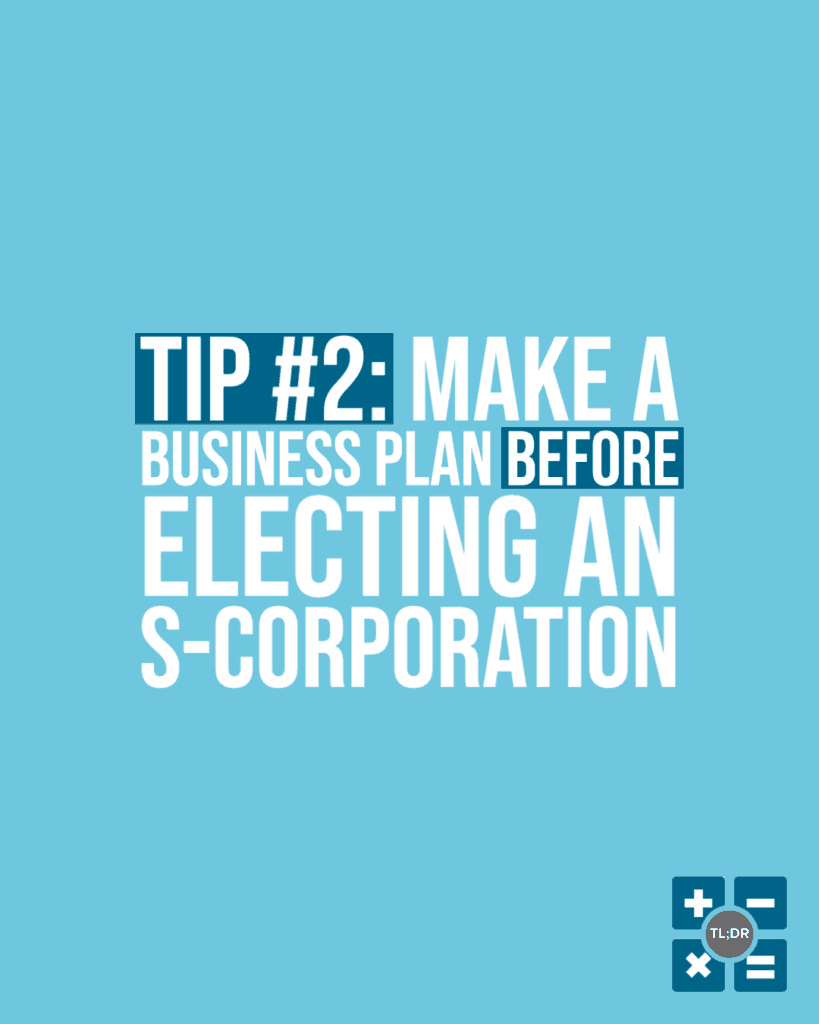

- While not a requirement, it is recommended that you form a business plan. What are your goals for your business, and how do you plan to achieve them?

- Pick a name! Not just any name though: your corporation’s name has to be unique.

- You can go here to find the names of companies that are already registered in the state of Washington (you don’t have to create a login, just scroll down below the login bit).

- If you’re worried about all the good names being already taken, just keep in mind that you can always add extra words to a name to distinguish yourself. If Smith Consulting is taken, maybe you can be H. R. Smith or Smith Financial Consulting or Smith & Smith Consulting.

- Don’t worry too much about being “boxed in” by a name. You can use what’s called a “DBA,” which stands for “Doing Business As.” This can also help if the nature of your business changes over time. Filing and using a DBA is rather simple, and you can even have multiple DBA’s.

- Choose the state in which you want to incorporate/ become an LLC.

- If you are doing all the paperwork yourself, you’ll probably want to file in your home state.

- There are certain states in the US that provide different benefits depending on what kinds of advantages you want your company to have. At the time of writing, Wyoming is pretty attractive for several reasons, but the differences in state law are beyond the scope of this article and subject to change.

- File articles of incorporation. For Washington State you can do this here, keeping in mind that there are plenty of online legal services that can cheaply file your articles of incorporation on your behalf for a fee.

- If you are incorporating in a different state from where you live, outsourcing the establishment of your corporation to a legal firm, or you simply want help with the paperwork involved in owning a corporation, you can choose a registered agent. The registered agent receives notices from the government on behalf of you and your corporation.

- Draft bylaws for your corporation. This is one of the formalities of owning a corporation that does not apply with less formal types of business. Basically, bylaws are the instructions for running your corporation.

- Register for an EIN (Employer Identification Number) here. Remember that all S-Corporations have at least one employee, because you are an employee.

- Obtain the required licenses and permits for your corporation. For a Washington State corporation you can go here to determine what you need based on your type of business.

- Appoint a board of directors, and hold your first board meeting. The agenda for your first board meeting should include:

- Adopting the Articles of Incorporation

- Selecting corporate officers

- Issuing stock

- Approving the S-Corporation tax election

- Determine the local, state, and federal filing requirements for your corporation. Or, you can have us keep track of all those things for you.

Congratulations, your S-Corp is formed! However, your work isn’t done there. As an S-Corp, you’re expected to follow a set of rules specific to S-Corps.

What Are the Rules You Must Follow When Accounting For S-Corp?

Okay, so you’ve formed your S-Corp. What is expected of you now? Let’s list out the rules that you and your corporation must follow:

- Pay yourself and the other owners of the S-Corp a reasonable salary.Learn how to do that here. This is a much-discussed issue and it gets a lot of people into trouble.

- As an S-Corp owner, when it comes to compensation you, frankly, have plenty enough rope to hang yourself. Since you are also an employee, you are in the unique position of determining your own salary.

- There’s a strong incentive to grossly underpay yourself, because if you pay yourself peanuts, you only owe payroll taxes on the peanuts, and the rest of your compensation (which you take as a distribution) doesn’t have that burdensome 15% self-employed payroll tax on it!

- Unfortunately, there are no hard-and-fast rules on how much you are required to pay yourself. BUT the IRS has the authority to determine if you are underpaying yourself, and they can charge fines, fees, penalties, and interest on any back-taxes you may owe if they think you underpaid your payroll taxes.

- Thankfully, there are experts, such as TL;DR: Accounting, who have read case studies and IRS rulings on reasonable compensation. If you’re in doubt about how to compensate yourself, just ask us and we’ll give you our recommendation.

- File your permits, licenses, and taxes on time. Now’s a good time to look them up and put renewal or filing dates on your calendar. Most government agencies will remind you when a filing or tax is due soon, but ultimately it’s up to you to remember when, where, and what to file in order to avoid penalties. Again, we can help you with this.

- You can only file one class of stock, you can only have US citizens or permanent residents as stockowners, and you can only have up to 100 shareholders. For the record, a family can count as one shareholder for this requirement.

- Keep minutes for your board meetings! If the IRS ever audits you, they will want to see your meeting minutes.

- What are meeting minutes? Meeting minutes are formal documents that record the date and time of meetings, participants, issues discussed, actions taken, votes, and any other pertinent information.

- By forming an S-Corporation, you are taking responsibility for ensuring that your corporation follows all the formalities required of you. This includes documenting and keeping records of meeting minutes. If you don’t have any meeting minutes, then it’s possible that you will lose your liability protection.

Be wary: if you do not follow the rules of being an S-Corporation, the IRS can reclassify you as a C Corporation against your will, and you will lose the unique tax benefits of S-Corporations!

If you have questions about taxes, bookkeeping or s-corporations that we didn’t answer, don’t hesitate to reach out. That’s what we’re here for!