As a child, did you look forward to how glorious a college degree was going to be, how it was going to open doors for you, or how it was a golden ticket to success? For much of the 20th century, a college degree was a golden ticket. Nowadays so many people have degrees that they don’t provide the kind of competitive advantage they used to.

At the same time, college tuition has grossly outpaced inflation. For as long as we can remember, we’ve shared jokes about how expensive college is, and rightly so! According to the Education Data Initiative, tuition has risen 747.8% since 1963, and that’s after adjusting for inflation.

Combining both of these ideas explains our ballooning nationwide college debt crisis. Millions of Americans are deep in debt incurred on the promise that they’d find a dream job that would make it easy to pay off this debt. But for many borrowers, even those who did get their dream job, there just isn’t enough money to cover rent, food, gas, and substantial student debt payments.

It doesn’t help that real wages have barely budged in decades.

The good news is that President Biden has announced a three-part plan to provide relief to these millions of Americans who are trapped between heavy debt and light wages. We’ll split this article into three parts of the plan: One-time debt relief, the pause on federal loan repayments, and provisions for those on income-based repayment plans.

Student Loan Forgiveness Plan: Debt Relief of $10k – 20k

The debt relief provision is quite generous for people who qualify for it. Unfortunately, these provisions do not phase out: They are all-or-nothing. Below is a simple if-then list that lets you see your total benefit eligibility. The maximum amount of debt relief, of course, cannot exceed your total debt owed.

- If your income was below $125k (single, MFS*) or $250k (MFJ* or HOH*) during either 2020 or 2021, you qualify for debt relief. Otherwise, you will receive no debt relief.

- Your loan(s) must be federal student loans.

- If you received a Pell Grant in college and your loan is held by the Department of Education, your debt relief maximum is $20,000. Otherwise, your maximum debt relief is limited to $10,000.

* MFS is Married Filing Separately, MFJ is Married Filing Jointly, HOH is Head of HouseholdCertain government and non-profit employees are eligible to have their entire federal student debt forgiven after making 120 qualifying loan payments. There are temporary special provisions of this new Plan that expire at the end of this October that allow some borrowers to receive loan forgiveness sooner than otherwise possible. Please see the official website for more information.

A Pause On Loan Repayment

The Biden Administration is making one “final” extension to the pause on all federal student loan repayments. This pause is effective until the end of 2022. It is not necessary to sign up for this repayment pause — the extension happens automatically.Note that this repayment pause does not apply to private student loans. Unfortunately, the federal government does not have the same power over private loans as it does on federal student loans. This can be especially painful for borrowers who were unable to qualify for federal student loans due to the income of a parent or guardian — the federal government assumes a parent or guardian’s wherewithal and inclination to pay for a child’s tuition based solely on annual income.

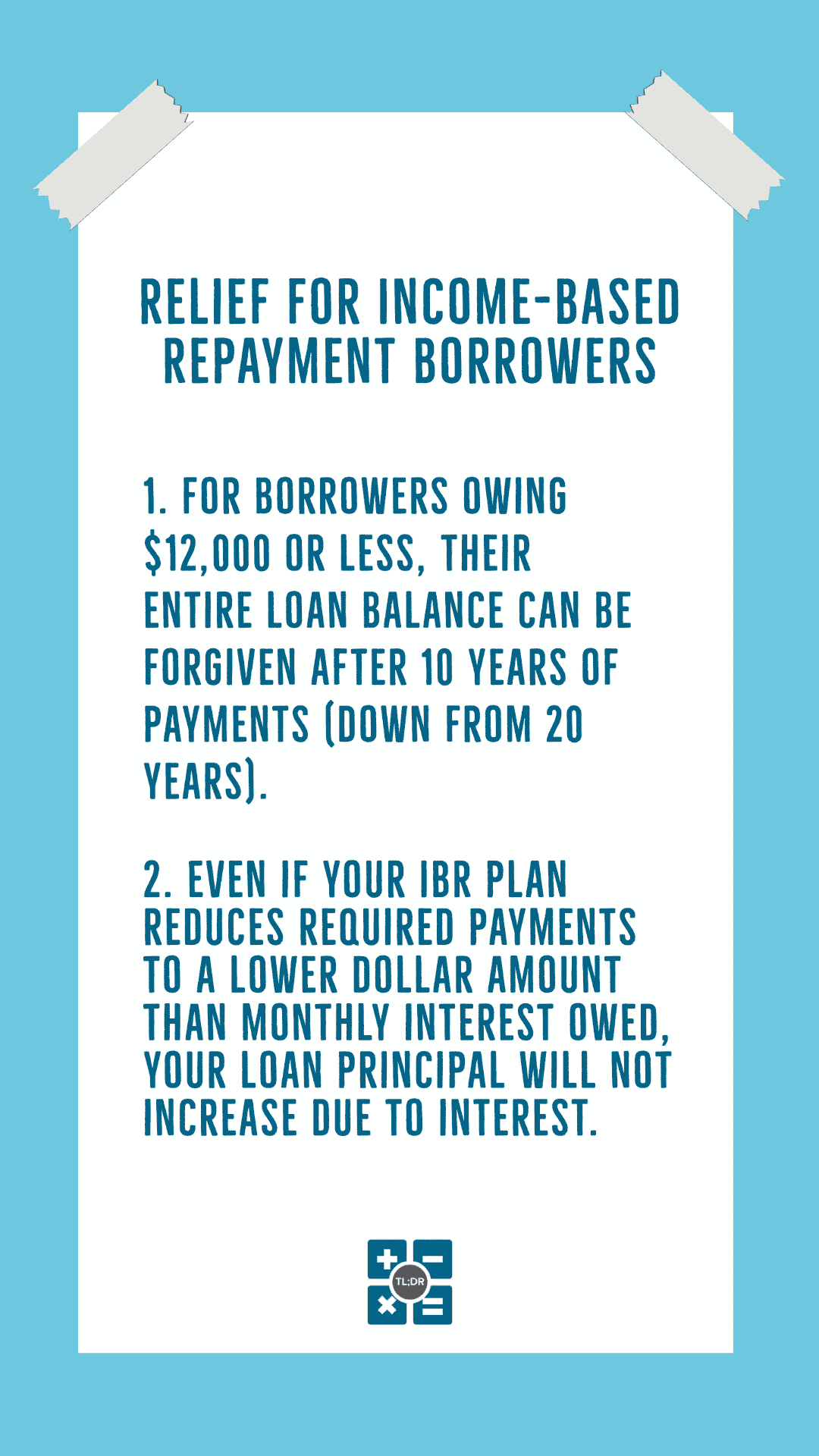

Relief for Income-Based Repayment Borrowers

Borrowers who are on an Income-Based Repayment (IBR) plan are now only required to pay a maximum of 5% of their discretionary income towards undergraduate loans. This is down from 10% of discretionary income. There is a new formula for calculating discretionary income which will result in a reduced amount. If you are on an IBR plan, you can expect your required payments to drop to less than half of what they were before (all else being equal).

There are two other provisions to make life easier for IBR borrowers:

- For borrowers owing $12,000 or less, their entire loan balance can be forgiven after 10 years of payments (down from 20 years).

- Borrowers will find that, even if their IBR plan reduces required payments to a lower dollar amount than their monthly interest owed, their loan principal will not increase due to interest (the federal government will cover the difference if the monthly interest exceeds your required monthly payment, even if your required payment is $0).

While there are many borrowers who will receive reduced benefits or no benefits due to their financial circumstances, this Student Loan Forgiveness Plan will help millions of American borrowers who feel buried under student loans regain more control over their own lives. We at TL;DR Accounting believe that everyone deserves a fair shot at success, and we feel that this plan will help ensure that many more of our fellow citizens have that chance.[Special note: For official updates, please sign up on StudentAid.gov here.]

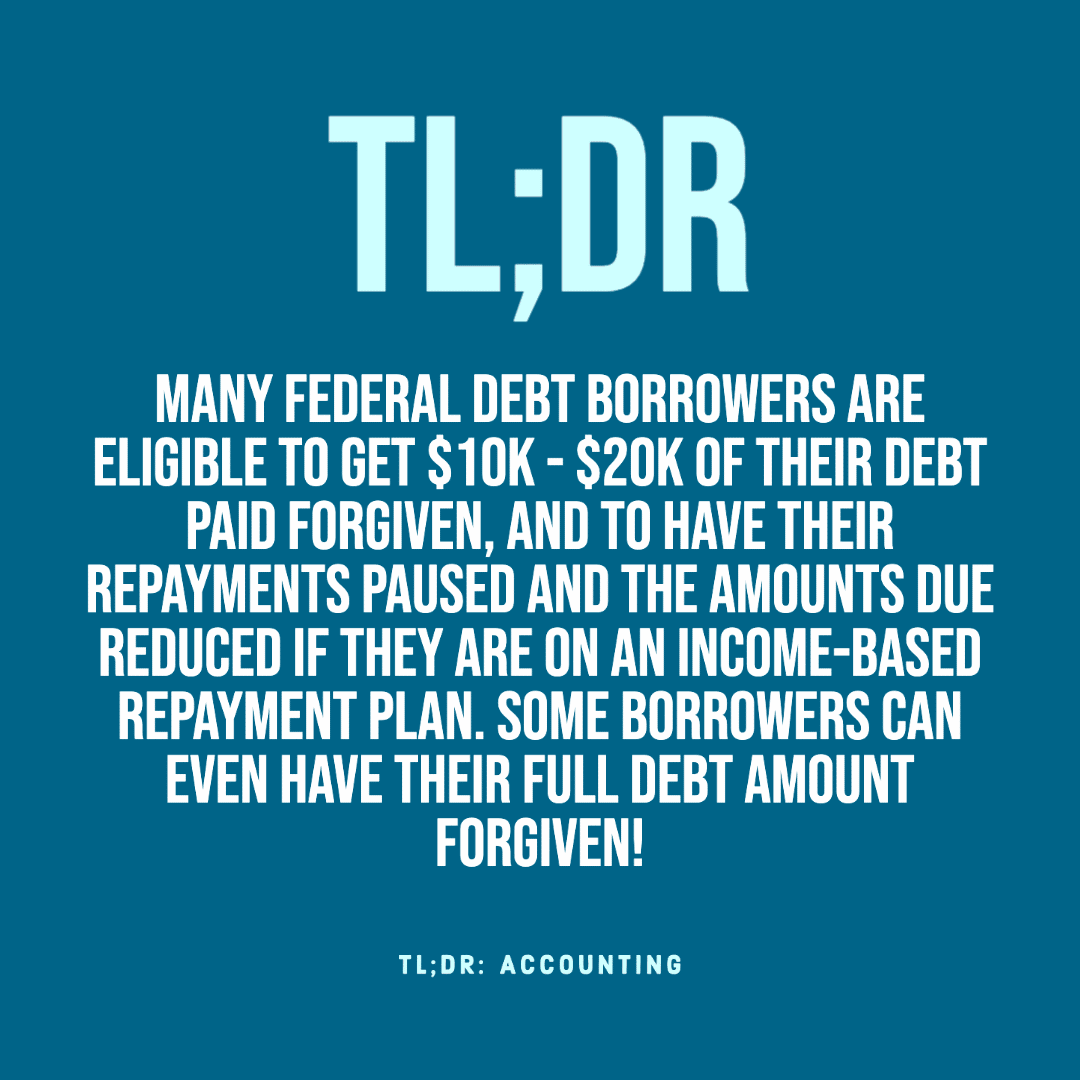

TL;DR: College is crazy expensive — and has been for many decades — contributing to massive student debt nationwide. Thankfully, many federal debt borrowers are eligible to get $10k – $20k of their debt paid forgiven and to have their repayments paused and the amounts due reduced if they are on an income-based repayment plan. Some borrowers can even have their full debt amount forgiven! We recommend that everyone who may qualify for any of these benefits sign up for email updates from the federal government here.