If you think of health insurance as a way to protect yourself from medical expenses “attacking” you, there was a time in America when employer-provided insurance was like a tower shield. For those who haven’t played many fantasy-themed role playing games, a tower shield is exactly what it sounds like, a shield so big that it towers over your body. An intrepid paladin could plant a tower shield in front of her and be secure in knowing that she’s not going to get hit by any stray arrows.

Insurance in the 21st century is not a tower shield. A decent policy might be more like a kite shield (which is not as big), and then there are some of us with a high-deductible catastrophic policy that is more like a tiny buckler — it will protect us from the worst of a staggering sword attack, but it won’t save our knee from a low-flying arrow.

Because a full-coverage “tower shield” medical insurance plan is mostly a thing of the past these days (unless you’re a congressperson), the best thing you can do is to armor up in different ways. A Flexible Spending Account (FSA) and a Health Savings Account (HSA) are two ways for you to protect yourself. These two plan types have major differences between them, but they have one important thing in common: they are tax-advantaged ways to cover “gaps” in your medical insurance. Perhaps their biggest benefit is that they help to pay for expenses before you’ve hit your deductible.

Sadly, you cannot use an HSA or FSA to pay for your health insurance premium, which these days might even exceed the amount you spend on health care in a year.

Let’s get into the details of both HSAs and FSAs, and end with a quick summary list.

The Health Savings Account (HSA)

A Health Savings Account functions as you might expect from the name. It’s a way for you to put money away tax-free so that you’ll have a “health nest egg” available to cover unexpected health expenses (or, for those of us who must regularly purchase high-cost pharmaceuticals, this money can cover expected health expenses).

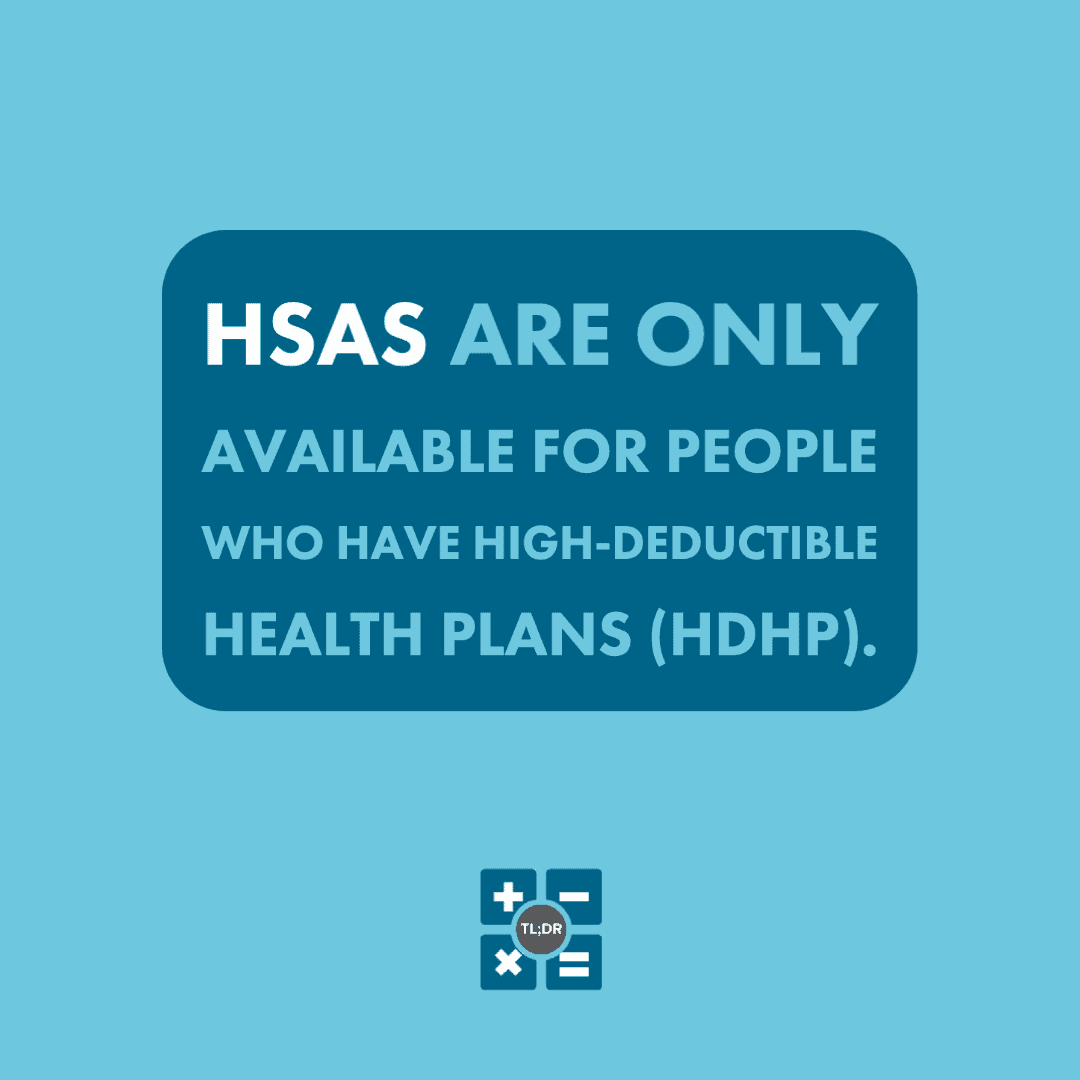

HSAs are only available for people who have High-Deductible Health Plans (HDHP). Specifically, the IRS defines an HDHP as a health plan with an individual deductible of $1,400 or a family deductible of $2,800. These numbers might seem a bit out of touch with reality, since $5,000+ deductible health plans are commonplace these days.

Well, that means that quite a few Americans qualify for an HSA. If you are in doubt, your health insurance plan should specify whether or not it is “HSA-eligible.” If you are unsure, you can contact your employer’s Human Resources office or a representative of your insurance provider.

You are only eligible for an HSA if all of the following are true:

- Your HDHP is your only health insurance plan, and it is HSA-eligible

- You are not eligible for Medicare

- You cannot be claimed as a dependent on someone else’s tax return

Your employer may have an established HSA for its employees, but note that you are able to set up an HSA for yourself regardless. Indeed, you can establish an HSA for yourself even if you are self-employed.

Tax advantages

Now, we mentioned above that an HSA is tax-advantaged. In this case, the tax advantage is that you do not have to pay income tax on HSA contributions. If you are an employee, your HSA contributions can be pulled from your paycheck and put into your HSA “before” they get taxed. Self-employed individuals can back the income taxes out of their HSA contributions come tax time.

HSA funds are only for eligible health expenses. This means that those funds can grow year over year and not be taxed if used for health expenses. This is a great strategy to put away money for health care expenses. If you spend HSA funds on ineligible expenses, you must pay income tax plus a 20% penalty tax, though the penalty tax does not apply if you are disabled or age 65 or older.

For 2021, the maximum amount that you can contribute to an HSA is $3,600 for individual coverage or $7,200 for a family. If your employer has an HSA plan, they may contribute to your account. In this case, your employer gets the tax break for their contributions. You only get to deduct your own contributions.

The Flexible Spending Account (FSA)

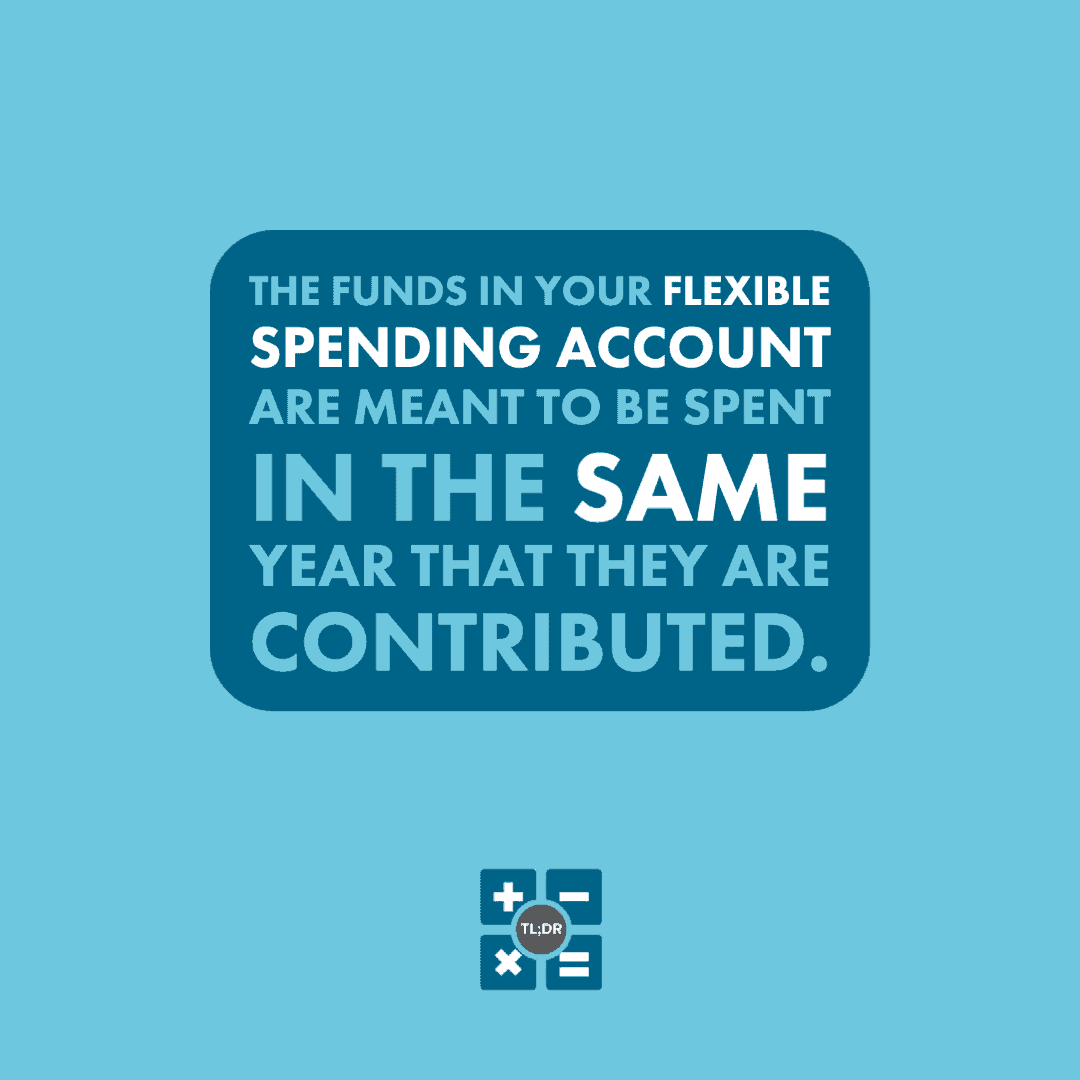

The Flexible Spending Account, or FSA (often called a “Flex Spending Account”) approaches the goal of easing medical expenses in a different way. Like an HSA, an FSA is also a way to avoid paying income taxes on funds you use to pay for medical expenses. Importantly, note that this is called a Flexible Spending Account. The funds in this account are meant to be spent in the same year that they are contributed.

Indeed, FSA accounts have a built-in “use it or lose it” policy. Originally, any unused funds in your FSA at year-end were lost, and the employer would keep these funds and was allowed to use them for administration of the program. Note that an FSA plan is an employer plan — you are unable to set up an FSA for yourself.

Nowadays, if your employer’s plan allows it, you can “roll over” up to $550 from your FSA to the following year. Any amount over this $550 limit is permanently lost to your employer. Alternatively, your employer may give you a special 12-month grace period to use your FSA funds, but this is a temporary measure due to COVID.

Generally, employees are eligible to sign up for their employer’s FSA regardless of health care plan, Medicare eligibility, or dependent status. If you choose an HSA, though, generally you should avoid also using an FSA for medical expenses.

While this post is mostly about medical expenses, note that employers can offer an FSA for dependent care benefits which maxes at $5,000 per year. Since dependent care is so expensive in most parts of this country, it is often worth maxing your contribution if you expect to have one or more children in childcare for the whole year. You can use an FSA for dependent care expenses whether or not you have an HSA or FSA for medical expenses.

The maximum contribution to a medical FSA for 2021 is $2,750. Note that this is higher than the rollover, so even if your employer has a rollover policy you could stand to lose up to $2,200 if you max out your contribution and don’t use any of it.

FSA funds must be used for eligible expenses. There is no official IRS-mandated penalty for using your FSA funds for non-eligible expenses, but you may face consequences from your employer if you use your account for unapproved expenses.

Your employer may decide to contribute to your FSA. This is worth taking into account when you figure your own contributions — be wary of your account growing to an amount larger than you expect to use this year!

Review: HSA vs. FSA

Going back to our shield-and-armor analogy: Health insurance is your shield. An HSA is your plate mail that you can use year after year until it’s used up. An FSA is more like hide armor that will disintegrate at the end of the year regardless of whether it faces any wear-and-tear during the year, except that you might be able to save a single leg-piece to spare you from buying a full set next year.

Note that in most cases you can’t have both an HSA and an FSA. The hide armor is too bulky to wear under your plate mail.

Pros and Cons of Both

HSA:

- Your employer may have an HSA set up, or you can set one up for yourself

- You must have a High Deductible Health Plan (HDHP) to be eligible

- Your documentation or a representative can specifically tell you if your plan is “HSA-eligible”

- You must not be eligible for Medicare

- You must not be a dependent on someone else’s tax return

- Maximum annual contribution is $3,600 (individual) or $7,200 (family)

- There is a hefty penalty for using contributed funds for non-eligible expenses

- Contributed funds do not expire

FSA:

- FSAs are set up by employers — there is no option to set up an individual FSA.

- There are very few restrictions on which employees can sign up for an FSA. Unless you are a business owner, you are likely eligible.

- Maximum contribution is $2,750 per year.

- If your employer offers a dependent care FSA, you can sign up for it and contribute up to $5,000 per year, whether or not you have a medical HSA or FSA.

- If you expect to have one or more children in child care for the whole year, it will likely cost more than $5,000. In this case we recommend maxing out your dependent care FSA.

- If you use your FSA for non-eligible expenses, you may face consequences from your employer.

- Contributed funds expire every year! But…

- Your employer may allow a $550 rollover, or

- Your employer may allow a grace period, but

- Your employer is not required to offer a rollover or a grace period!

TL;DR: These days, many insurance plans have dizzyingly-high deductibles. What’s a taxpayer to do when they have $5,000 worth of annual medical expenses but their deductible is $6,000? Enter HSAs and FSAs. These are ways to use your earnings to pay for medical expenses without that money being subject to income tax. HSAs are nest eggs for current or future health expenses, and you can set one up for yourself even if you are self-employed. Medical FSAs can only be set up by an employer, and they are for current medical expenses, as in, you should only contribute money to an FSA if you are pretty sure you will use it this year. Unspent FSA contributions may be permanently lost to you at the end of every year. Whether or not you have an HSA or medical FSA, you may benefit from an employer-run dependent care FSA.